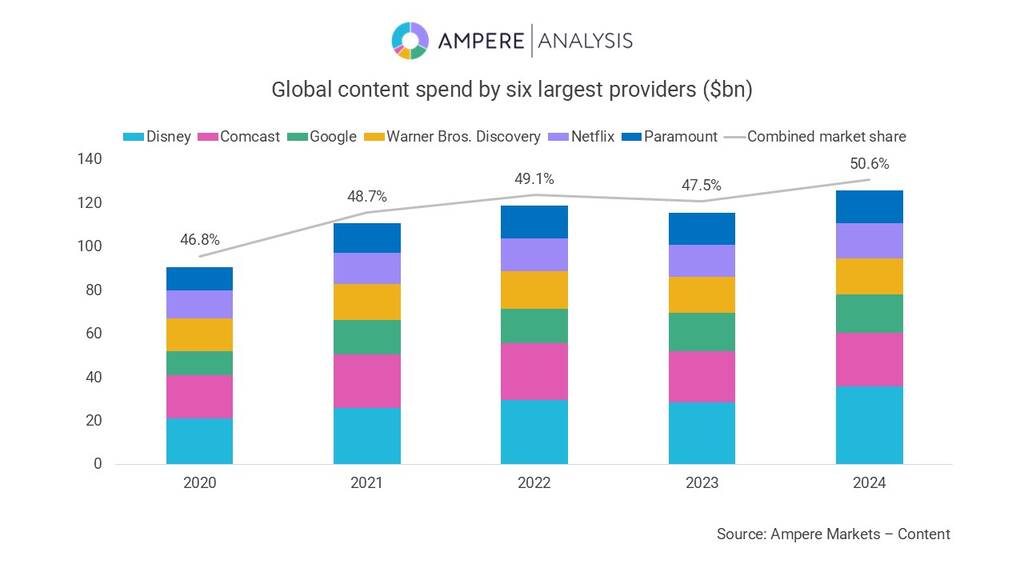

Top six global content providers – Disney, Comcast, Google, Warner Bros. Discovery, Netflix, and Paramount – will invest a combined $126bn in content this year.

According to research by Ampere Analysis, the spending across these groups will reach a new high in 2024 and account for 51% of the total content spend landscape, up from 47% in 2020.

Despite announced cutbacks amongst its linear and theatrical brands, Disney remains the largest contributor to the media landscape at 14% of global investment in TV and film content in 2024. This has been supported by the full acquisition of Hulu at the beginning of 2024, adding an additional $9bn in to Disney’s spend total.

Original content spend remains the leading spend type across the six providers, accounting for over $56bn in investment and 45% of their total spending since 2022.

Google’s contribution to the content market comes via YouTube, and investment in programming through its revenue-sharing arrangements with content creators. YouTube continues to build its global presence through partnership deals with major content owners, making it the third largest contributor to the content landscape.

Netflix is the top investor in global streaming content, averaging a total of $14.5bn in annual investment in original and acquired programmes since the pandemic. Further growth is expected in 2025 through the acquisition of Sports Rights for NFL matches and WWE entertainment.

In total, $40bn of the $126bn is currently spent on these six operators’ subscription streaming services, including Disney+, Peacock, and Paramount+. Ampere said this highlights the growing importance of these platforms as audiences move away from linear television in favour of the convenience and expansive catalogues available via streaming.

Peter Ingram, Research Manager at Ampere Analysis said: “Ongoing investment by major studios and streaming platforms into new programming will continue be key to keeping audiences engaged and entertained. We can expect that the content landscape will see low level growth in 2024 as production schedules recover from disruptions caused by the pandemic and the writers’ and actors’ union strikes. Looking forward however, while these top six providers will continue to account for the majority of spend, overall growth will plateau as companies look to refocus their output. This will include limiting commissioning volumes and prioritising strategic investments and profitability to counter the current challenges of the media market.”

You are not signed in

Only registered users can comment on this article.

Netflix uses GenAI on 300 titles in 2026

Netflix has revealed that nearly 300 titles on its platform have used generative AI, from early concept stages and pre-visualisation through to post-production and release.

Poppy Dixon appointed BBC Head of Documentaries

The BBC has appointed former Sky executive Poppy Dixon as its Head of Documentaries.

Virgin Media launches AI robots to monitor TV network in real-time

Virgin Media has created its own AI robots to monitor its television network quality in real-time in a bid to quickly identify and resolve any issues when they occur.

US government seizes over 1,000 websites streaming FIFA World Cup

Global anti-piracy coalition the Alliance for Creativity and Entertainment (ACE) has applauded the US government’s seizure of over 1000 illegal websites streaming the FIFA World Cup over the past month.

Channel 4 names Simon Rexworthy as Chief Strategy and Corporate Development Officer

Simon Rexworthy has been named Channel 4’s Chief Strategy and Corporate Development Officer. He will report to Chief Executive Priya Dogra and join the broadcaster’s executive committee.