Home

Watch

IBC2026

IBC Daily

Log in

Enter keywords

Submit search

Watch

IBC2026

IBC Daily

Accelerating Innovation

Accelerating Innovation

IBC Accelerators

Tech Papers Hub

Intellectual property

Artificial Intelligence

Artificial Intelligence

AI Audio

AI Post-Production

Deep Fakes & Digital Replicas

Ethics

GenAI

Machine Learning

Scraping & Training

Connective Tech

Connective Tech

5G

6G

Cloud

Digital Audio Workstation

Edge Computing

IP Workflows

Network Slicing

IBC Show

IBC Show

IBC2024

IBC2023

IBC2025

Immersive Tech

Immersive Tech

AR

Immersive Audio

Metaverse

MR

Spatial Computing

Volumetric Video

VR

XR

OTT & Streaming

OTT & Streaming

AVOD

CDNs

FAST

SVOD

TVOD

People & Purpose

People & Purpose

Acquisition & Retention

Diversity, equity & inclusion

Skills & Training

Sustainability

Production

Production

Audio Tech

Camera Tech

Content Acquisition

IP Production

LED Volumes

Live Production

Outside Broadcast (OB)

Remote Production

Sports Production

Storytelling

Studio Production

Virtual Production

Virtual Production

Camera Tracking

Worldbuilding

Motion Capture & Performance

Rendering & Compositing

Robotic Cameras

Enter keywords

Submit search

Monetisation

E-Commerce

Topics:

Ad Sales

Data Analytics

E-Commerce

Product Placement

Rights Management

Subscription Management

Choose a topic

Ad Sales

Data Analytics

E-Commerce

Product Placement

Rights Management

Subscription Management

View other themes:

CHOOSE THEME

ACCELERATING INNOVATION

ARTIFICIAL INTELLIGENCE

CONNECTIVE TECH

IBC SHOW

IMMERSIVE TECH

OTT & STREAMING

PEOPLE & PURPOSE

PRODUCTION

VIRTUAL PRODUCTION

News

Sure bets for monetisation with Magnaquest

Read now

News

Vivendi plans London listing for Canal+, Amsterdam float for Havas

News

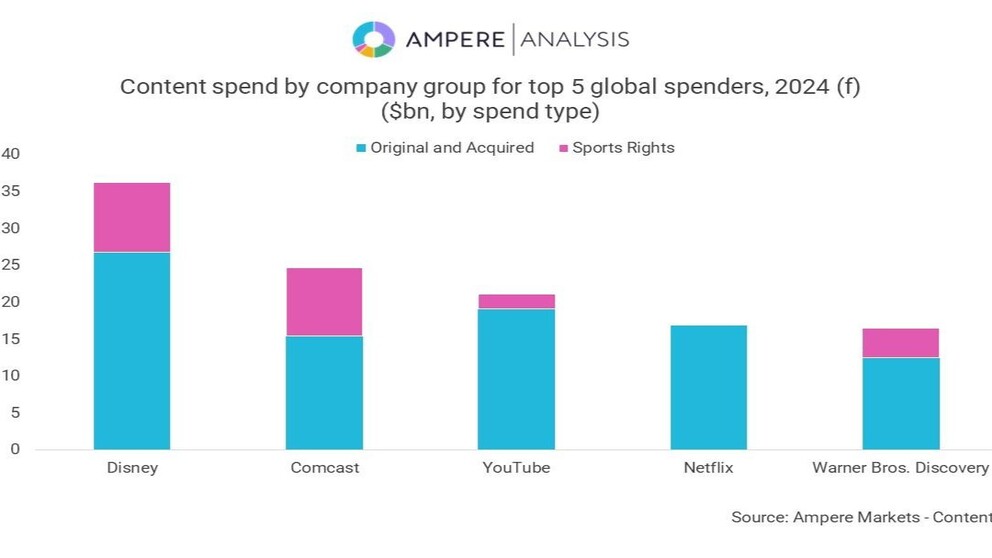

YouTube ranks second for non-sports content spend, says Ampere report

News

Sony Pictures Television acquires majority stake in Eleventh Hour Films

News

BBC to explore licence fee reform says Director General Tim Davie

News

Eastern Europe OTT revenues to climb 82% by 2029

News

BBC announces Small Indie Fund recipients

News

Barbie Crowned Top UK Home Entertainment Title of 2023

News

IMG’s 2024 Trends: Smart Stadiums, AI and Monetising Women’s Sport

Features

The Era of Media Consolidation is Not Over

News

Netflix Ad Tier Hits 15m Monthly Users

IBC Show VOD

On the money: How to choose a monetisation model

Interview

AiBuy: in-content shopping solution

News

IBC2023: Dynamic growth in AVOD revenue ahead

News

IBC2023 Keynote: Evan Shapiro - ‘Dinosaur’ media businesses must adapt

News

Hasbro sells eOne to Lionsgate for $500 million

News

Vice completes $350 million sale to former lenders

Features

Local content hits home for SVODs