The transition to HD has been one of the most important media technology spending drivers in Europe in the last decade.

Broadcasters upgraded their infrastructures right across content production and delivery to allow for HD capture and transmission.

This drove a significant wave of spending that fuelled media technology suppliers’ growth, particularly in the period 2009-2012 – as demonstrated by IABM DC GMVR historical figures.

The transition to HD has now reached maturity although HD channels continue to be launched, for example as a result of the cable digitisation in Northern Europe, and HD spending continues on replacing equipment installed up to a decade ago that is now reaching the end of its useful life.

Recent figures indicate that most viewers now rely on HDTV, which has become mainstream in European households.

The media technology community has been waiting for the same to happen to UHD.

UHD formats include increased pixel resolutions (4K, 8K), higher frame rates (HFR), higher dynamic range (HDR), wider colour gamuts (WCG) and/or their combinations – UHD enhancements such as HDR and HFR can also be added to HD broadcasts.

UHD has been considered to be the next natural upgrade for broadcasters.

Several media technology suppliers have therefore invested heavily in developing UHD-capable products to take advantage of the potential wave of investment by broadcasters.

“Although UHD take-up is still slower than expected, Europe is faring better than other regions when it comes to UHD deployments”

This has translated into increased R&D spending. However, the number of channels launched has been below the expectations of the supply community – particularly with regards to UHD.

High R&D spending coupled with low adoption by customers has in turn translated into increased pressure on margins for suppliers that had bet heavily on UHD – this has been highlighted in several IABM reports.

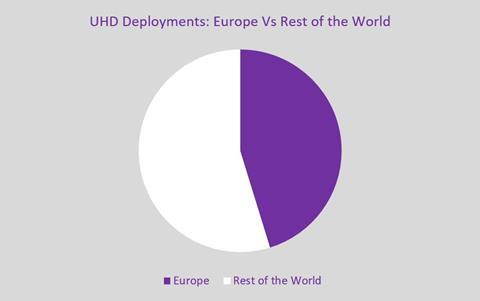

Despite the lower than expected take-up of UHD, Europe can be considered as the territory where more UHD initiatives have been launched.

IABM looked at UHD Forum’s data – last updated in April 2017 - on UHD deployments around the world and found that almost half (45%) of the services launched are European initiatives. Asia-Pacific has 31% while North America only 20%.

This shows that, although UHD take-up is still slower than expected, Europe is faring better than other regions when it comes to UHD deployments.

Most UHD channels have been launched by pay TV operators. This can be easily seen by looking at the European countries that boast the highest number of UHD initiatives in the UK and France.

In the UK, BT and Sky launched 4K initiatives in the summer of 2016.

BT launched its 4K/UHD service on IPTV, which covers live sports including the UEFA Champions League and the Premier League, in August 2016.

Sky started broadcasting sports, films and TV shows in 4K/UHD via satellite from August 2016 as well through its Sky Q technology (above).

In France, IPTV operators such as Orange France and Free launched 4K offerings between 2015 and 2016.

Orange launched a 4K offering featuring sports and Netflix programming in 2016 while Free started carrying a 4K channel – Festival 4K - focused on music festivals, concerts, entertainment events at the end of 2015. Other 4K offerings in France were launched by Fransat and SFR on satellite and IPTV respectively

Commercial and public broadcasters have not gone beyond broadcast trials in the higher resolution format – and/or occasional broadcasts for special live events.

This is due to the low added revenue potential of UHD in commercial broadcasting as opposed to Pay-TV. In fact, the presence of UHD channels in Pay-TV bundles can constitute a subscription and therefore revenue driver while the same does not apply to a commercial setting – i.e. advertising inventory’s value is generally uncorrelated with image resolution.

This constitutes the main difference between HD and UHD in Europe so far. While HD rapidly rose to mainstream status and became the de facto quality format for both commercial and subscription-based broadcasters, UHD so far remains a niche market for Pay-TV operators.

If we break down the UHD Forum’s data further, this becomes clearer. Some 88% of UHD deployments in Europe have been launched by cable, IPTV or satellite operators with IPTV being the most popular platform.

This is different from North America where a striking 64% of initiatives have been launched through OTT services. This difference translates into different types of services in the two continents: live prevails in Europe while VOD is prevalent in North America.

It is highly uncertain that this will change. Several commercial broadcasters pressured by stagnant advertising growth are prioritising efficiency considerations in broadcast and media technology purchasing over resolution upgrades.

IBC2017 IABM will show new data on UHD adoption by broadcasters from the biannual IABM End-User Survey at the IABM State of the Industry Conference Session on the 15th of September.

This new data on UHD will also feature buyers’ preference over UHD enhancements such as HDR, HFR and WCG.

It will be interesting to see if European buyers are more or less interested in these enhancements – which can be added to HD broadcasts too – than they are in 4K-only broadcasts.

Also, the data will show how broadcasters plan to deploy UHD, for example preferred infrastructure and compression standard for deployment.

Attendees at the session will also receive a copy of the new edition of the IABM Business Intelligence Digest, including a Regional Focus on Europe.

No comments yet